Uniform Residential Loan Application (URLA) Form

Loan officers, processors, and brokers • Standardize borrower intake • Reduce missing fields • Clear section-by-section flow • Easy to customize

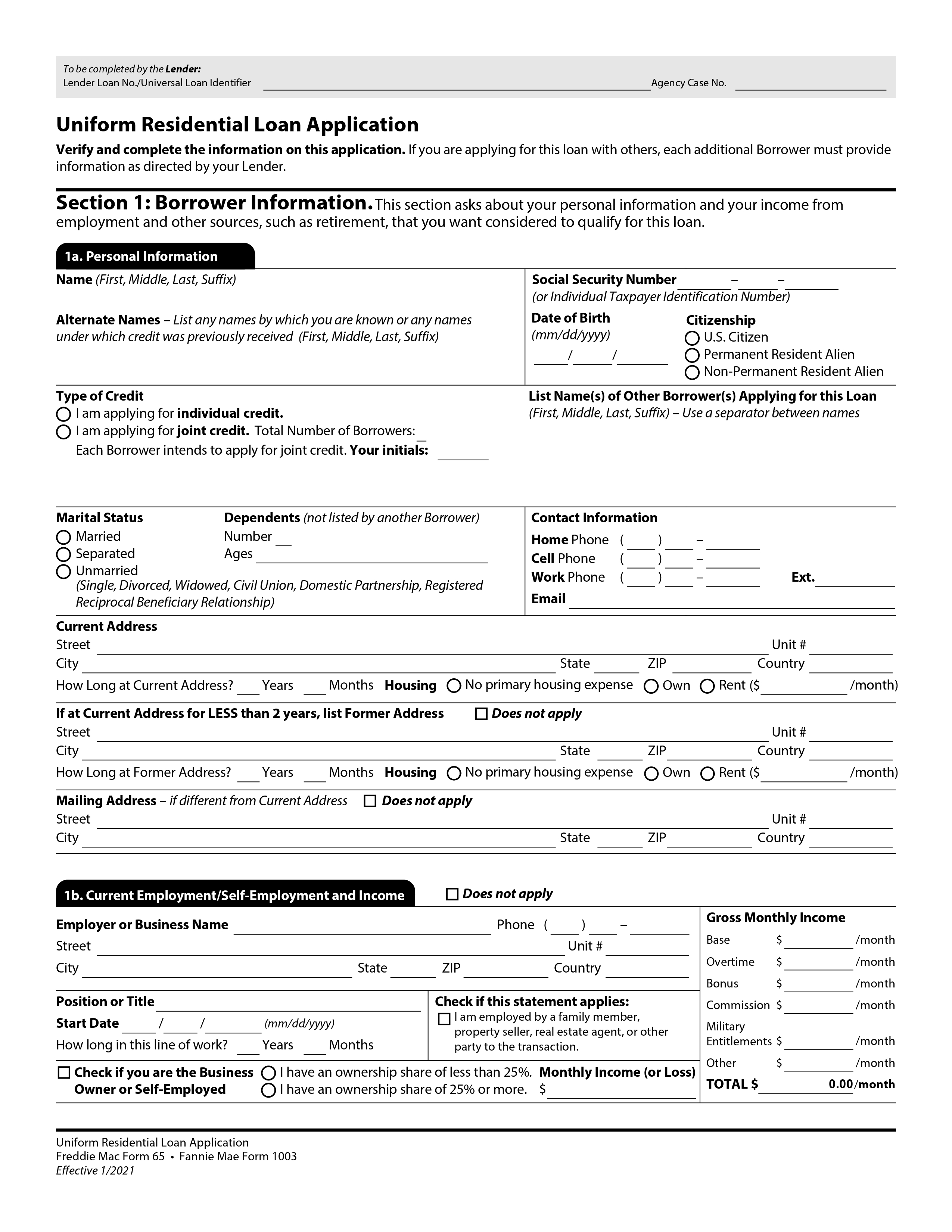

Use this Uniform Residential Loan Application (URLA) form template to collect borrower details in a consistent, lender-ready format. It mirrors the standard Freddie Mac Form 65 / Fannie Mae Form 1003 flow so loan officers, processors, and mortgage brokers can capture borrower identity, employment and income, assets and liabilities, real estate owned, loan purpose and property details, and required declarations—reducing back-and-forth and preventing missing fields that slow underwriting.

Key Benefits

Common Use Cases

Frequently Asked Questions

What is the Uniform Residential Loan Application (URLA)?

Do borrowers have to provide demographic information?

What information should be gathered before completing the URLA?

Is the URLA the same for purchases and refinances?

Checklist

Lender Use

Often completed by the lender after file creation.

Borrower Information

Use the exact legal name that will appear on closing documents.

Include prior names used for credit history.

Used for identity verification and credit review.

Use mm/dd/yyyy format.

Select the appropriate category as directed by the lender.

If joint, list all borrowers and confirm initials as required.

Dependents should not be duplicated across borrowers.

Capture best contact for follow-ups and verifications.

If renting, include monthly rent.

Many lenders require a 2-year housing history.

Use when the borrower receives mail elsewhere.

Employment and Income

Employer name, address, phone, position/title, and start date.

Complete if the employment is connected to the transaction.

Indicate ownership share and business owner status if applicable.

Use gross monthly income amounts as directed by the lender.

Use when the borrower has multiple jobs or income sources.

Include start and end dates and prior income when required.

Other Income

Only include items like alimony/child support if the borrower wants it considered.

Assets

Include account type, institution, account number, and value.

Add credits relevant to the transaction as needed.

Liabilities

List company, account number, unpaid balance, and monthly payment.

Include only if applicable to the borrower’s monthly obligations.

Real Estate

Refinance files typically list the subject property first.

Complete for each property when the borrower owns real estate.

Loan and Property

Confirm the purpose matches the file and disclosures.

Primary residence, second home, or investment property.

Answer based on how the property will be used and constructed.

List additional liens when there are multiple loans.

Used for 2–4 unit or investment properties when required.

Include source and whether funds are deposited.

Declarations

Answer all questions accurately; attach explanations as needed.

If yes, provide details when requested by the lender.

Acknowledgments

Borrower should review obligations and authorization language before signing.

Sign and date using the required method (electronic or wet signature).

Military Service

Complete when the borrower or surviving spouse has service history.

Demographic Information

Borrowers may choose not to provide; follow lender instructions.

Loan Originator

Typically completed by the loan originator and organization.